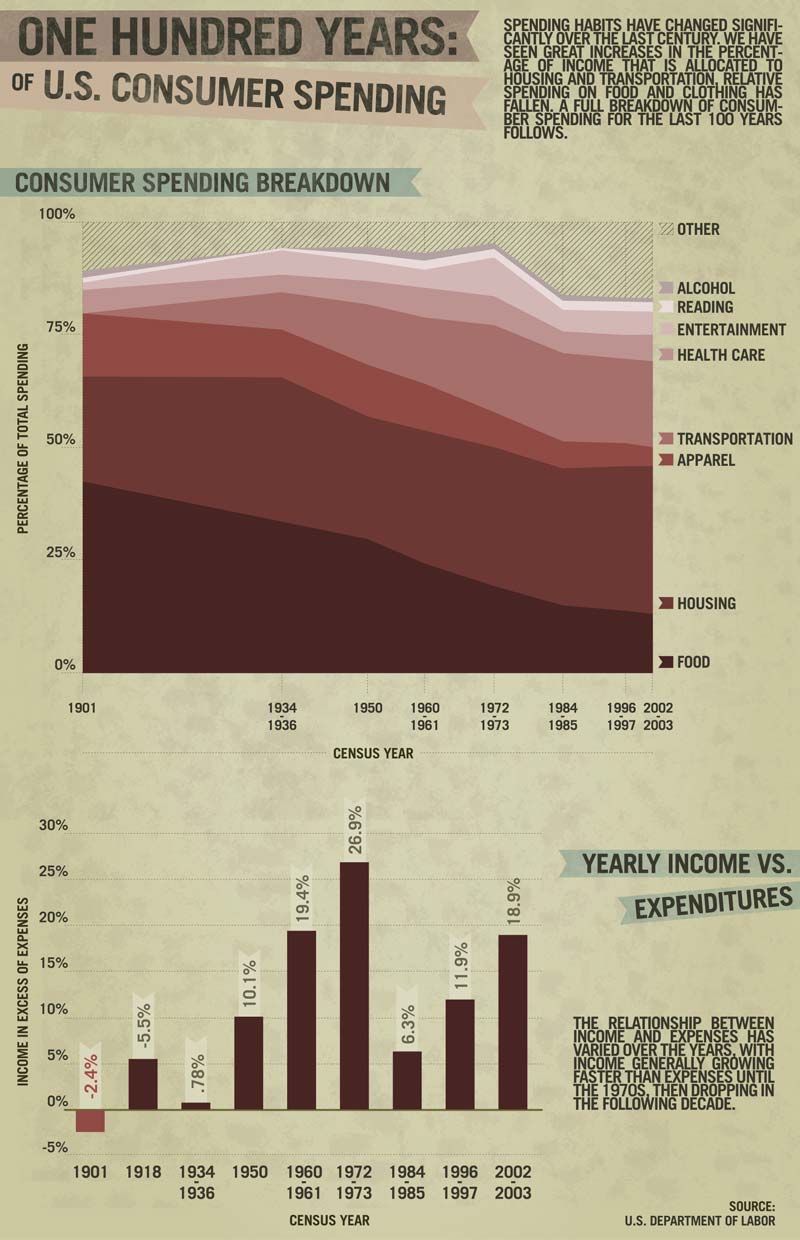

March 30th, 2010 by Christian

Time and again in American politics, Republicans have voted as a unit to frustrate our disorganized Democratic majority. No matter what's on the table, a few Democrats will peel away from the party core; meanwhile, all Republicans will somehow manage to stay on-message.

Thus, they caucus block us.

. . .

Articles noting this phenomenon anecdotally

appear all the time, and despite the recent hopeful spate of Democratic victories, the fact that Republicans form an exceptionally effective opposition party is undeniable. Today, we're going to perform a data-driven investigation of this—and discover some fascinating things about the American electorate along the way. Our data set for this post is

172,853 people.

I should start off by pointing out that the Left/Right political framework we're usually handed is insufficient for a real discussion, because political identity isn't one-dimensional. For example, many Libertarians have Left-leaning ideas about social policy, and Right-leaning ideas about personal property. Where do they fit on a single ideological line?

There are

many methods of looking at the political spectrum, but the best way I've come across is to hold social politics and economic politics

separate, and measure a person's views on each in terms of

permissiveness vs.

restrictiveness on a 2-dimensional plane. Like so:

As you can see, I've superimposed some 'party' labels, to add some real-world context. One could quibble with the names I've chosen, but I feel that, in a broad sense, they fit: Democrats have a permissive social outlook and believe in restricting the financial sector (through regulation); Republicans essentially believe the reverse. In their corner, Libertarians would like to end restrictions across the board, and, down in the lower right, we have people who prefer that all aspects of life be guided by some authority: religion, the government, whatever.

. . .

Now, with the definitions out of the way, we can get to some information. We'll begin with the most basic measurement: people's economic and social values. Because our data set is so comprehensive, we can even measure the change in these values with age.

Politics is a big part of dating, and we've gleaned this post's data from

OkCupid's question database. Our sample size today is 172,860 people.

These lines contain a neat little story:

- Both socially and economically, teenagers prefer an anything-goes type situation.

- But as these teenagers grow up a bit and enter the job market, they quickly develop progressive economic ideas: perhaps a bit of "levelling" seems pretty good when you're staring up the professional ladder from the bottom rung. Meanwhile, their youthful live-and-let-live social philosophy begins to fade.

- In their late 20s, they start making real money. Economic progressivism goes out the window, preferably out the window of a building with a doorman. As the adult mind turns to more material matters, social views don't change that much.

- Finally, after the mid-40s, retirement looms. Our former teenagers check their collective 401(k)s and think, you know what, let's all get checks from the government. Social views take a hard turn for the more restrictive. At the end of the journey, economic and social views are again in agreement—only this time on the other side of the philosophical line!

Anyhow, these numbers

really come alive when we take the next intellectual step and

plot social and economic beliefs together as an ordered pair. So doing, we can get a picture of how the the average total political outlook evolves over time.

Now, with this picture in hand, we can go a step further with our data. The American two-party system creates an interesting mathematical situation: we can bisect our political plane

a two-party system allows us to bisect the political plane and see which party more closely reflects a given age group's ideology simply by asking which side of the line the group lands on. People sitting in the upper right half should vote, in theory, for Democrats. People in the lower left, for Republicans. Like so:

The Implication of Our Two-Party System

But of course this line assumes that social and economic values are

equally important to a person and that his or her priorities don't change as time goes by. Obviously, neither is the case in the real world. So let's see exactly how those values change and do even more with our graph.

Digging deeper into

OkCupid's matching database, we find the following

new information on people's political priorities:

The way this data bears on our political plane is mathematically cool, but

arctan(x) really has no place in a political discussion (except in

Flatland!), so I'll just summarize by

a change in political priorities causes our

dividing line to rotate saying a shift towards either social or economic issues causes our Democrat/Republican dividing line to

rotate about the center of our political plane. Here's exactly how it happens; this timeline is basically the sum of all the information we have shown so far. Use the slider to step through time.

The Effects Of Changing Political Priorities

age

From this animation, we can consolidate all that we've learned about each group into a single plot. The blue dots are the ages likely to vote Democratic, the red are the Republican ones. In case you're keeping score, there are

21 blue dots and

22 red ones.

People's Ultimate Political Tendencies

This detailed portrait of the electorate jives well with the actual exit poll numbers from the last few Presidential elections.

The New York Times has collected this data

and present it very well, if you have time to take a look. Here's the part that concerns us:

To wind up this section, I'd like to take one last look at our political plane, with a final set of overlays that I think are most illuminating:

The polygons I've drawn over the dots are called

convex hulls; they are a geometric way to measure the spread of a set of points. In this case, the hulls tell us the size of the ideological/age base of our political party.

As you can see, the Democrat's base is much larger. And the range of political values it encompasses is vast. Here's party-to-party comparison in tablet form, for easy digestion:

Unlike in many things, size here is a liability. Yes, a political party that's this wide-open is probably a more intellectually stimulating organization

ideological size is a liability to be a part of, and it has a lot more

potential power. But bigger base is also just that many more competing viewpoints Democratic politicians must cater to and that many more different viewpoints in play among the actual elected officials themselves.

Also, well over half of the Democratic party's hull lies

outside of its upper-right-hand ideological home, implying that you've got many groups of people who might tend Democratic, but who have disagreements with the party on particular issues and could defect, should the slant of the party or the country tilt the wrong way. On the other hand, the Republicans are concentrated in the lower-left-hand corner. This red cluster has

multiple, apparently self-reinforcing, reasons to vote with their party, giving the Republicans both a more fervent power base and a little more ideological wiggle-room along either the social or economic axis.

So when you read about

the thousands of Catholic nuns who recently came out in favor of health care reform, it's easy to get excited about being a Democrat. But do you think those same people will side with us on things like gay marriage? Or abortion rights? Hull no!

. . .

That's the crux of the problem: Republicans cohere, Democrats don't. After the above mathematical dissection of the political plane, let's take our conclusion in hand and see how it plays with other dating data we have.

This whole Republican/Democrat situation reminds me (as it surely reminds you)

I think of Mamluks sometimesof when Napoleon and his few French divisions dispersed the vast Mamluk horde by the banks of the Nile. Like an army, a political party must be

coherent and

disciplined to be effective, and these qualities alone can carry the day, even against greater numbers.

Let's look at ideological distributions on a few hot-button issues and see how the Democrats are spread out and exposed. We'll start with views on abortion. This chart shows the opinions of

social conservatives and

social liberals. Everything is as you'd expect: liberals are pro-choice; conservatives pro-life.

Now let's look at how

economic liberals and conservatives view abortion:

Again, the

conservatives are strongly pro-life. But the

economic liberals have

widely distributed views. A solid portion of the Democratic economic base actually sides with Republicans on this issue. It's those nuns again!

While the two conservative curves are nearly congruent, the liberals ones are totally different. The takeaway, the Republican advantage, is this: economic conservatives and social conservatives agree, while the liberal halves of these spectra don't. Furthermore, the purple overlap—in a sense "the swing vote"—is largely on the conservative side!

We see same pattern repeated again and again. Here, for example, is a look at the 'Gay Marriage' issue:

. . .

Finally, I want to wrap up this burrito with a look at

OkCupid's specialty: matching people up.

Below are two matrices, showing person-to-person

match percentages. These numbers are a measure of how well two people get along. We've used them to facilitate over 100,000

marriages in the last few years; their accuracy is well-tested. Match percentages range from 100 (awesome) to 0 (terrible), and the site average is

61.

We excluded explicitly political questions, ran numbers for the different ideologies, and found these patterns, which I'll leave you with:

As you can see, conservatives of both stripes get along with each other better than liberals do with themselves, even on

non-political issues. We calculate match percentage by posing a series of questions to our users. Just to give you a sense of what these questions are like, here are the top three most important (by user vote):

1. If you had to name your greatest motivation in life so far, what would it be?

- Love

- Wealth

- Expression

- Knowledge

2. Which makes for a better relationship?

3. Are you happy with your life?

I find groupthink frightening. But that fact that Democrats can't get together on some multiple-choice Q & A, speaks volumes about why they struggle with the infinite possibilities of government.